As you draft the lease for your new store, finalize a business loan, or issue shares to new investors, you might think that it is just a simple signing of documents and filing them right away. But, there is one tax obligation that quietly risks many Micro, Small, and Medium Enterprises (MSMEs), making most business owners know about it only when a Bureau of Internal Revenue (BIR) audit notice comes in.

It’s called the Documentary Stamp Tax (DST).

Probably, you may never have heard of it, or you are not really sure which of your documents require it — do not worry, you are not alone. Indeed, DST is one of the most overlooked tax obligations, and non-compliance carries penalties.

This guide will break down what you need to know about DST and how you can stay compliant.

What is the Documentary Stamp Tax?

Documentary Stamp Tax (DST) is an excise tax imposed on specific documents or instruments that serve as proof of acceptance, assignment, sale, or transfer of an obligation, right, or property.

In other words, when you execute a document that creates a legal or financial relationship among parties, the government requires a tax to be paid. Regardless if a document is electronic, it is still subject to DST.

Moreover, DSTs are transaction-based, arising from the moment that a covered document is executed.

For MSMEs, DST commonly arises from everyday business transactions such as:

- Entering or signing a lease agreement for your office, warehouse, or store

- Taking a bank loan or business credit

- Entering into a contract of sale for real property or shares of stock

- Executing promissory notes, deeds of assignment, or mortgages

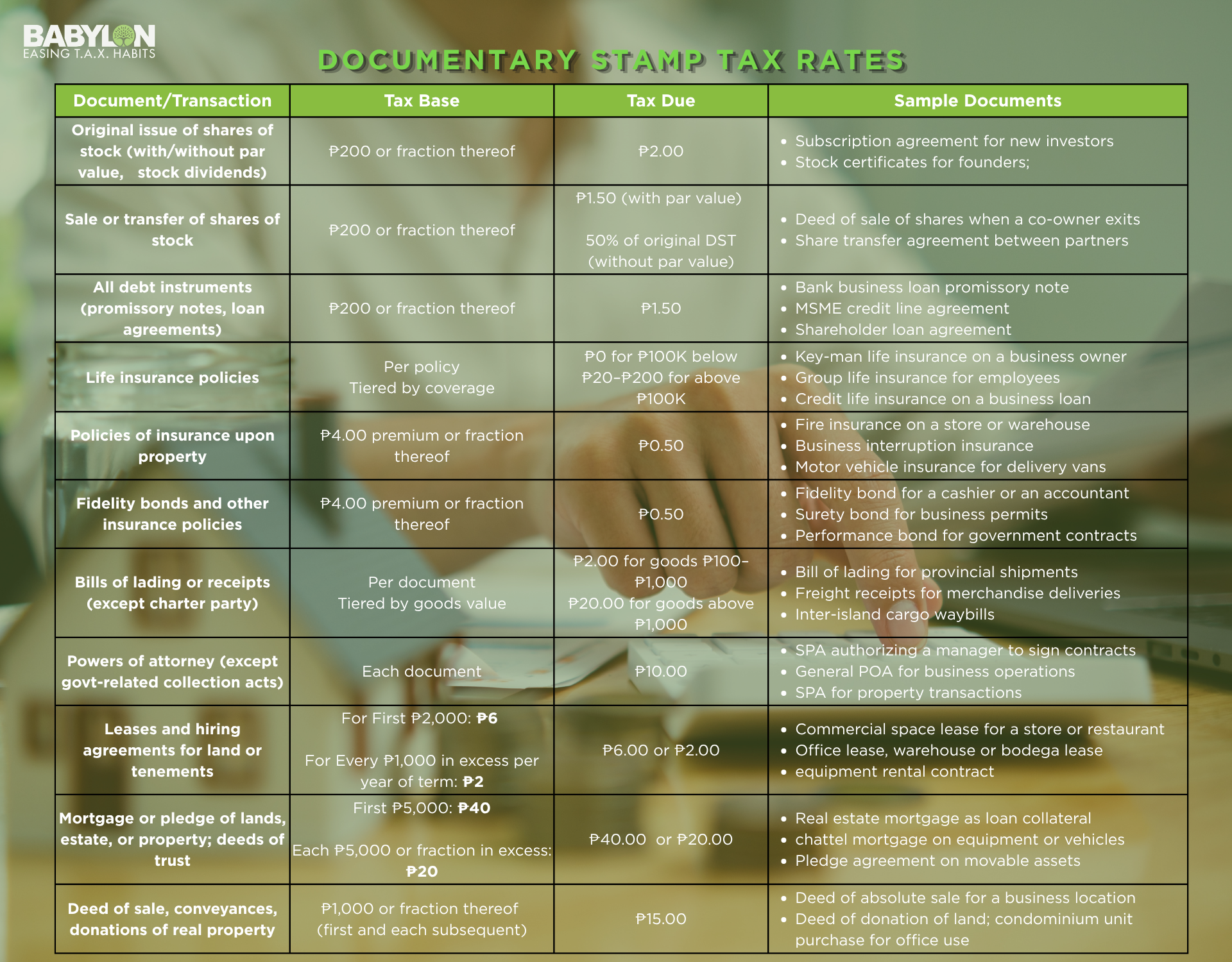

DST Rates That Apply to Your Business: A Practical Reference Table

Here are the tax rates most relevant to Philippine MSMEs and sample documents for their business that are subject to DST:

Who Pays DST: The Buyer, the Seller, or Both?

Under the provisions of the National Internal Revenue Code (NIRC), the DST is paid by the person making, signing, issuing, accepting, or transferring the document. An exception to this is when a party in a document has an exemption from DST, the other party that is not exempt shall be liable for the said DST.

For MSMEs, here are some of the common conventions:

- Lease agreements: commonly shouldered by the lessee or tenant, though parties can agree otherwise

- Loan documents: borne by the borrower

- Sales of property or shares: the seller, though the contract can stipulate otherwise

- Service contracts: the party issuing the document is liable

When and Where to File DST

The DST is remitted to the BIR using BIR Form 2000 or Documentary Stamp Tax Declaration Return, and/or BIR Form 2000-OT Documentary Stamp Tax Declaration Return ( for One- Time Transactions)

- Filing Deadline: the DST must be complied with on or before the 5th day after the close of the month when the document was made or executed. For example, if you executed a lease agreement on March 15, 2025, the DST must be filed by April 5, 2025.

- Filing Channels: It shall be filed with the Authorized Agent Banks (AABs) within the jurisdiction of the corresponding Revenue District Office (RDO). In case of no AABs, it shall be filed with the Revenue Collection Officer within the RDO.

Common DST Mistakes MSMEs Make

Here are some of the common mistakes to avoid regarding DST compliance:

- Assuming that your Bank or Counterparty has already filed: Never assume such a filing. Always confirm in writing who is responsible for compliance and keep a copy of BIR Form 2000 as proof.

- Forgetting DST on Notarized Contracts: Notarization does not substitute for DST compliance. Thus, an unstamped document will be non-compliant with BIR requirements.

- Overlooking Informal Lending Transactions: even loan agreements between family, friends, or fellow business partners that are reduced to writing are covered by DST if they fall within the NIRC’s provisions.

- Misfiling Forms for DST: Since there are two forms for DST, it is proper to know which form applies to your transaction type.

- Not keeping DST receipts for Audit Purposes: Since the BIR can audit you, ranging from 3 years back or up to 10 years in cases of fraud, it is better to keep all DST filings and payment confirmations organized.

On a Final Note

Documentary Stamp Tax may seem like a minor detail in the daily grind of an MSME, but the implications of compliance cannot be overlooked — as every document ignored can lead to a compounded liability that can destabilize your business.

The good news is that DST compliance is entirely manageable with the right systems and guidance in place.

At Babylon2K, we help Philippine MSMEs stay on top of tax obligations like DST, so you can focus on growing your business instead of worrying about BIR notices. Contact us today and let’s set up a compliance review for your business.

References:

- Tax Reform for Acceleration and Inclusion (TRAIN) Sections 174-197

- Revenue Regulations 4-2018

- Revenue Memorandum Circular 3-2018