The Audit Myth

For many business owners, the word “audit” triggers immediate anxiety. The common assumption is that audits are about catching fraud, exposing weaknesses, or triggering penalties large enough to threaten everything you have built.

If you are a Filipino MSME owner feeling this way, you are not alone – especially if the word first came up alongside a tax assessment. But avoiding audits because they feel threatening is a costly mistake.

This guide explains what auditing actually is, how it works, and why it protects your business more than it exposes it.

What Auditing Really Is

An audit is an independent, systematic examination of a company’s financial records and operations to determine whether its financial statements accurately reflect the state of the business.

Think of it as an annual business check-up. The specialist is not there to find fault; they are there to confirm what is working, flag what needs attention, and give you a credible basis for decisions.

In the Philippine context, audits follow the Philippine Auditing Standards (PSAs), the local adoption of the International Standards on Auditing. These standards ensure that financial statements comply with the Philippine Financial Reporting Standards (PFRS).

In short, the checklist confirms that your reports are accurate and credible to investors and regulators alike.

The Two Main Types of Audits You Will Encounter

- External Audit: Conducted by an independent Certified Public Accountant or audit firm hired by your business. This is the type most relevant to MSMEs, as it is required by the Securities and Exchange Commission (SEC) and the Bureau of Internal Revenue (BIR)

- Internal Audit: Conducted by in-house auditors who review your internal operations on an ongoing basis.

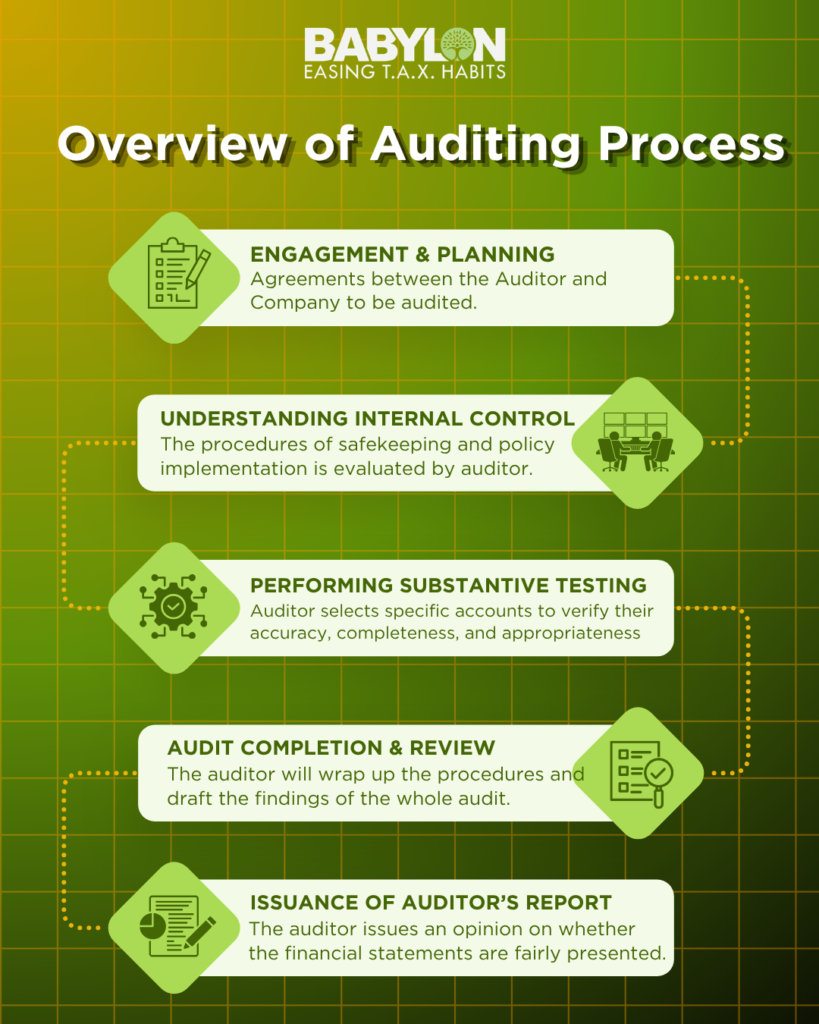

The Auditing Process: Step-by-Step

For an overview of the entire audit process, refer to the layout below.

Undoubtedly, understanding the whole process demystifies the essence of audit. Here are the in-depth details of the steps in auditing:

Step 1: Engagement and Planning

The auditor and the company agree on the scope, schedule, responsibilities, and fees through an engagement letter. The auditor then performs a risk assessment to identify which areas of the financial statements are most likely to contain material errors.

Key activities at this stage include reviewing prior years’ financial statements, contracts, board minutes, and other corporate documents, as well as setting materiality thresholds — the level at which an error becomes significant enough to affect a decision-maker’s judgment.

Step 2: Understanding Internal Controls

The auditor evaluates the company’s internal controls: the policies, procedures, and systems in place to prevent errors and irregularities. Strong controls reduce the extent of testing required; weak controls signal the need for closer scrutiny. Common areas reviewed include authorization policies, separation of duties, and bank reconciliation procedures.

Step 3: Substantive Testing

This is where most of the fieldwork happens. The auditor tests specific transactions and account balances for accuracy, completeness, and appropriate classification, using methods such as:

- Vouching: tracing journal entries back to source documents

- Confirmation: independently verifying balances with third parties of the company, such as banks and customers

- Analytical Procedures: comparing figures against expected amounts or prior periods

Typical areas tested include recognition of revenue, accounts receivable, inventories, fixed assets, accounts payable, payroll accounts, and related-party transactions. Note that auditors use sampling techniques, as it is not feasible to review all business transactions.

Step 4: Completion and Review

The auditor consolidates all findings, reviews them for consistency, and addresses any outstanding issues. This stage typically includes a review of subsequent events (events that occurred after the financial reporting date that could affect the financial statements), obtaining written management representations, and applying final analytical procedures to the financial statements as a whole.

Step 5: The Auditor’s Report

The audit concludes with a formal report stating the auditor’s opinion on whether the financial statements present a true and fair view of the company’s financial position.

There are four possible outcomes:

- Unmodified Opinion: Financial statements are fairly presented. This is considered the gold standard or clean representation of the company.

- Modified Opinion: Financial statements are mostly fair, with specific issues or exceptions noted.

- Adverse Opinion: Financial statements are materially misstated and unreliable for users.

- Disclaimer of Opinion: The auditor could not form an opinion due to scope limitations.

For MSME owners, an unmodified opinion is more than just a formality; it is a credential that tells banks, investors, and regulators that your numbers can be trusted.

Why Your Business Likely Needs an Audit

Auditing may seem like just another compliance cost, but consider what unaudited financials can cost you in practice:

- Bank Loans and Credit Facilities: Most financial institutions require at least 2 years of audited financial statements.

- SEC Annual Reporting: Corporations with total assets or liabilities exceeding ₱600,000 must file audited financial statements.

- Investor Confidence: Serious investors commit capital only where financial information is independently verified.

- Business Growth: Potential partners and franchisors need confidence in your financial position.

- Merger & Acquisitions: Business valuations require independently verified financial data.

The Hidden Cost of Skipping Audits

Many MSME owners think they are saving money by deferring audits. In practice, they are often accumulate a larger problem.

When audits are done reactively, such as when they are rushed to meet a bank deadline or regulatory cutoff, costs typically rise. More importantly, the underlying risks go unmanaged:

- Accumulated errors: Without independent review, disorganized records go uncorrected and compound over time.

- Undetected misstatements: Unverified books carry the risk of misrepresenting profitability, which can mislead your own business decisions.

- Regulatory exposure: Material misstatements can attract penalties from the SEC or the BIR, including for incorrect deductions or inadequate disclosures.

In Conclusion

Auditing is a vital component of every business. Regardless of size, every creditor, investor, and even customer deserves accurate financial information to ensure their safety and diligence.

Additionally, with audited financial statements, you can gain a clearer picture of your business and the knowledge you need to improve your operations. Later on, it can lead you to better opportunities and make you more competitive in your industry.

Here at Babylon2k, we work with small and medium-sized businesses in the Philippines to make financial compliance, including the audit process, manageable, understandable, and affordable.

Whether you are working with an external auditor of your choice or need guidance on finding the right audit firm for your business size and industry — our team is equipped to support you through every phase of the process. Just send us a message or schedule a free consultation, and together we can ensure your business is on the right track.