Running a business can sometimes be confusing, especially if you are a one-man army handling the operations. Indeed, you collect payments, pay your suppliers, cover the rent and utilities, & hire an accountant for your taxes.

Month after month, the numbers and documents pile up, and somewhere in those piles is information that either the Bureau of Internal Revenue or any regulatory agency will ask you to explain.

Most Micro, Small, and Medium Enterprise (MSME) owners view accounting as something to do after the business, like a year-end chore. But that approach quietly costs you, such as missed deduction claims, surprising tax assessments, cash flow problems, and the anxiety of not knowing if your business is really profitable.

Here is an important demystifying fact: your business follows a process, just like how you comply to your requirements when you are just starting things out. Similarly, it happens to accounting — called the Accounting Cycle, and we will simplify it for you.

What is the Accounting Cycle?

The accounting cycle is the whole process that your accountant or bookkeeper follows to record, organize, and make reports of every financial transaction you had in your business. Moreover, it covers the period from the moment you invest, make sales, pay expenses, and create financial statements.

You can think of it as an operating system that runs silently behind your business. Even though you may not see it, almost everything depends on it: Income tax return, VAT filings, credibility for loan applications, and alike.

For Philippine MSMEs, an appropriate accounting cycle typically means:

- Proper BIR Compliance: Your books can withstand scrutiny and file accurate tax returns

- Better Decision-Making: This is attainable because your figures reflect what is the reality

- Smoother Audits: Any audit done by an external auditor or tax assessment can flow easily

Additionally, the accounting cycle usually covers one accounting period — which usually depends on how you need it, like doing it on a monthly, quarterly, or yearly basis.

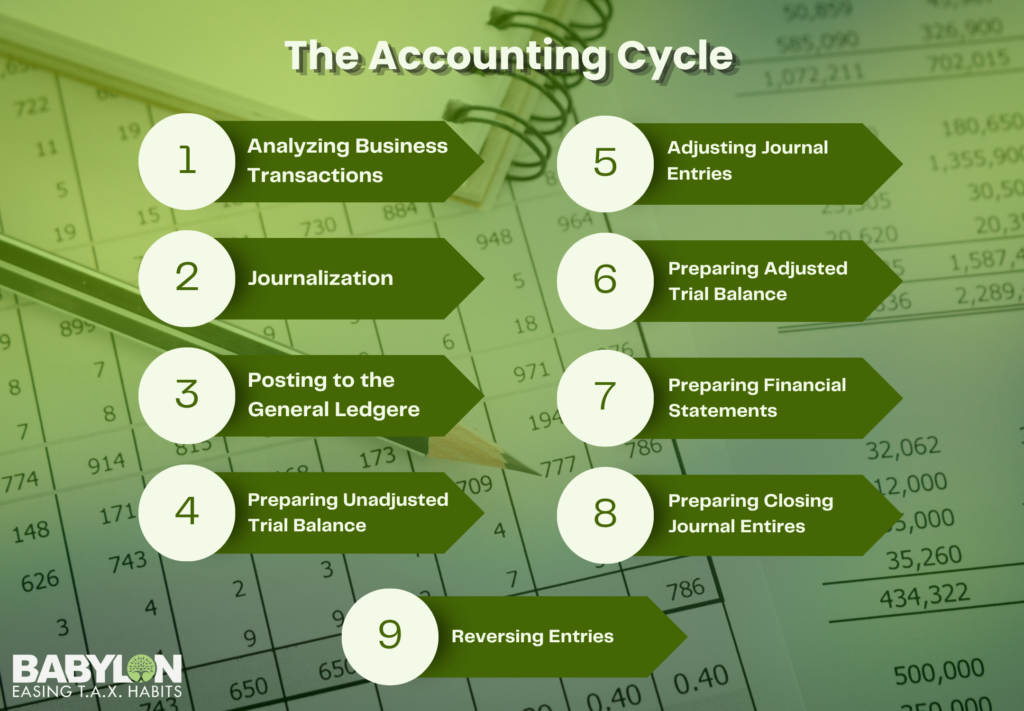

The 9 Steps of the Accounting Cycle

Let us walk you through the whole cycle by going through it step-by-step easily.

Step 1: Analyzing Business Transactions

It all starts with a transaction: either a sale, purchase, payment to a supplier, or a loan acquired. Before you record anything, make sure you identify and analyze what happened — which can be called an Accountable Event.

In relation to determining whether a transaction is an Accountable Event, you may need to answer these key questions:

- Did this event affect the business financially?

- Which accounts are involved?

- Does it either increase or decrease an asset, liability, equity, income, or expense?

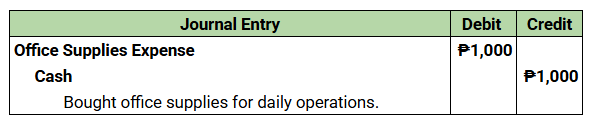

For example, as you purchase office supplies worth ₱1,000, there will be a decrease in your Cash (Asset Account) and an Increase in your Office Supplies Expense (Expense Account). Definitely easier than it sounds, but it may require some practice to get your analysis right, especially on some complex transactions.

Nonetheless, many small business owners skip this important mental step and just hand the documents to their bookkeeper. Having a basic understanding of what each transaction means can drastically help you avoid errors and prevent you from mixing personal and business expenses.

Step 2: Journalizing (Recording Journal Entries)

Once a transaction is properly analyzed and considered as an Accountable Event, it will be recorded in the General Journal using the double-entry system in bookkeeping.

Note that every transaction shall have two sides: A Debit and a Credit, and they must always be balanced. Additionally, a short explanation is included to clarify details on the said journal entry.

Using the same example regarding Office Supplies acquired:

This journal entry is the official first recording of a transaction. Whether you are using a manual ledger, Microsoft Excel, or Google Sheet, for accounting software such as QuickBooks and Xero — this step creates a document trail that any auditor or regulatory agency, such as the BIR, expects to see.

Undoubtedly, journal entries are the foundation of the succeeding steps in the accounting cycle. Any form of error here, such as confusing numbers or making a mistake on which one should be in the debit or credit side, will affect the entire financial reporting. Furthermore, official receipts, contracts, and other documents from the financial transaction get attached.

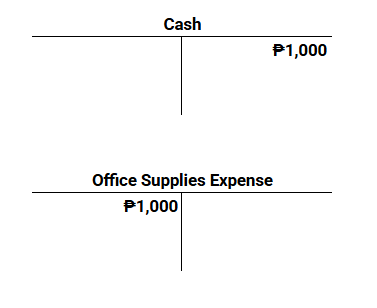

Step 3: Posting to the General Ledger

After journalizing all of your transactions, each entry will be posted or transferred to the General Ledger, which is the master record that contains all transactions and groups them according to the accounts involved.

You can think of it as moving each transaction from a list into individual account folders: one folder for cash, sales, accounts payable, and so on.

For simple representation, the T-Account can be utilized to show how the General Ledger, the left side of the T- Account, represents debits, and the right side represents credits. In addition, at the end of a period, each account in the ledger shows its total running balance.

Taking from the abovementioned example:

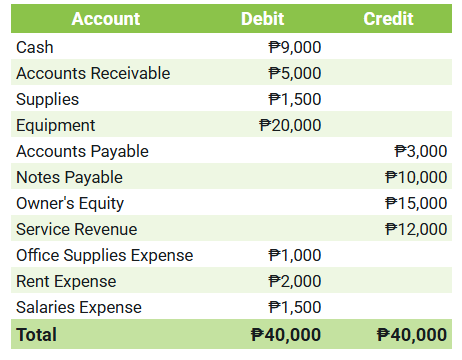

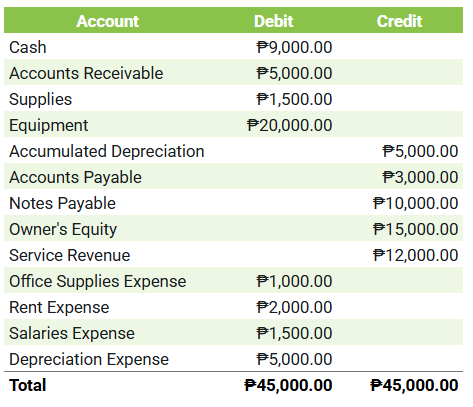

Step 4: Preparing an Unadjusted Trial Balance

Once everything is posted properly, the accountant will then prepare an Unadjusted Trial Balance. It is a list of all accounts with their ending debit or credit balance

The purpose of this document is to make sure that total debits will equate the total credits. If they were not balanced, something was posted incorrectly and needs to be fixed before moving forward.

The unadjusted trial balance serves as a checking point. Even if it does not guarantee 100% accuracy, you can still spot transactions recorded in the wrong accounts and catch mathematical errors early before they pile up into bigger issues.

Step 5: Adjusting Journal Entries

It is considered one of the most important and most misunderstood steps of the cycle is adjusting entries. They are made at the end of the accounting period to consider the transactions that have already incurred or occurred but have not yet been paid or recorded.

Common adjustments are:

- Accrued expenses: such as wages earned by employees or utilities pending but not yet paid

- Prepaid expenses: Rent paid in advance that spans multiple periods but has not been considered for the expired portions

- Depreciation: the gradual wear and tear of assets such as equipment

- Unearned revenue: Payments received from customers but have not yet delivered the services or goods they’ve ordered

Additionally, under the Accrual Basis of Accounting, these adjustments are a must. Thus, if these are skipped, the financial statements would not reflect what has truly occurred during the period. It can potentially lead to overstated or understated income, leading to incorrect compliance filings.

Step 6: Preparing an Adjusted Trial Balance

After doing adjusting entries and posting them, a second trial balance is done, called the adjusted trial balance.

With this trial balance, the financial statements can then be prepared, as it reflects the ending balances for the accounting period with regard to all accounts in the business.

Step 7: Preparing Financial Statements

This is the step wherein most business owners want — the reports themselves. With the adjusted trial balance, your accountant will prepare:

- Income Statement (Profit or Loss): It shows your revenue, expenses, and overall net income or loss during the period

- Balance Sheet (Statement of Financial Position): shows your Assets, Liabilities, and Equity

- Statement of Cash Flows: gives you a view of how cash moved in and out of the business

- Statement of Changes in Equity: reflects the movement of the owner’s capital account

Indeed, these are the most crucial documents whenever you file for compliance, such as to the BIR or SEC, and for acquiring potential lenders or investors.

Step 8: Closing Journal Entries

At the very end of the accounting period, Nominal Accounts (Temporary), such as revenue, expense, and drawing accounts, are closed or zeroed out. They must start fresh in the new upcoming period.

Subsequently, the balances are transferred to a Summary Account (Income Summary Account), and then to the Owner’s Equity or Retained Earnings account.

More importantly, the balances of the Assets, Liabilities, and Equity are not closed, as they are rather carried forward to the next accounting period.

Closing entries are crucial as they provide clarity on the income and expenses of each period. Without it, mixing of nominal accounts would occur, and it would be impossible to get a measurement of performance in the said period.

Step 9: Reversing Entries

The final step of the accounting cycle, and the one most people probably do not hear about, is Reversing Entries.

These are done at the beginning of the new accounting period, wherein they reverse a certain adjusting entry in order to be practical and simplify bookkeeping. Note that this is not mandatory and only an option, depending on what you prefer.

A good example of this is accrual of unpaid salaries to employees, such as a ₱15,000 unpaid balance. Your bookkeeper will reverse the corresponding payable and expense account so that when the processing of payroll occurs, you will avoid the double count of the expense.

Thus, reversing entries reduces the possibility of bookkeeping errors when actual transactions finally clear in the new accounting period. They are useful for businesses with regular accruals or complex payroll cycles.

What Happens When the Cycle Breaks Down?

Let’s face it: the accounting cycle would not always be running on a smooth manner, as receipts will get lost, entries may be overlooked, and year-end becomes a scramble puzzle to reconstruct months of financial transactions.

Without a doubt, the consequences are not just messy books; they are real business risks, such as:

- Tax Assessments: Since there are improper recordings, it may lead to underpayment of taxes and incorrect filings

- Inaccurate Financial Statements: Unreflected realities can result in cash flow problems and mistaken interpretations of the business as a whole

- Loss Opportunities: Due to inaccuracies and unnecessary time spent on fixing records, scaling up the business can be a lost opportunity.

Indeed, these are some of the reasons why MSMEs that partner with an experienced accounting firm just do not save time; they also protect their business from exposure.

Ready to Get Your Books in Order?

Whether you are just a startup or trying to clean up years of scrambled records, understanding the accounting cycle is just the first step. The next step is to make sure that it is being handled accordingly in full compliance with Philippine regulations.

Here at Babylon2k, we work with MSMEs across the nation to set up and maintain clean accounting systems that build confidence even when subjected to regulatory scrutiny.

Let’s talk about where your books stand — Reach out to us for a free consultation.