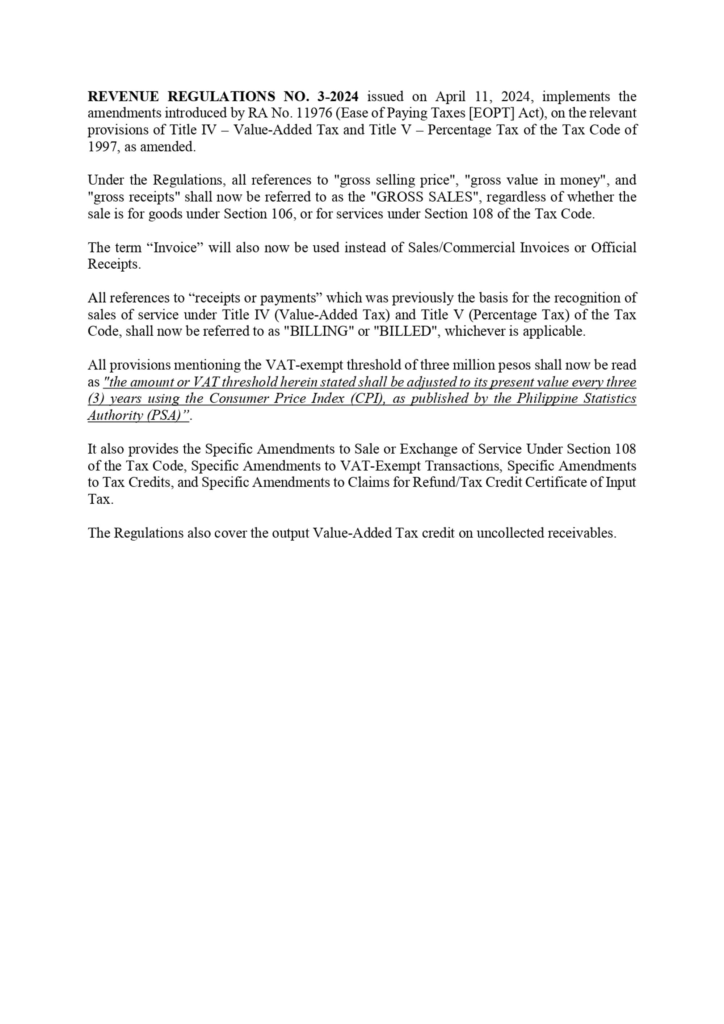

New Rules for VAT & Percentage Tax (A.K.A. EOPT’s VAT and Percentage Tax Timely Amendments)

“As the deadline for VAT filing approaches, embracing Revenue Regulation (RR) No. 3-2024 is not just compliance, it’s strategic business acumen,” says a leading accountant. RR No. 3-2024 simplifies and modernizes VAT and Percentage Tax under the Ease of Paying taxes (EOPT) Act. This regulation is set to simplify tax processes, reduce administrative burdens, and enhance transparency, making it easier for businesses to manage their tax obligations effectively.

Key Amended Provisions

Section 1: Scope

This section establishes the purpose of RR No. 3-2024, which is to implement amendments related to VAT and Percentage Tax as per the Ease of Paying taxes (EOPT) Act. This reflects a broader effort to streamline tax processes and reduce administrative burdens on taxpayers.

Section 2: Amendments

Five principal modifications are outlined:

- Gross Sales: The act shifts from recognizing sales on a cash basis to an accrual basis for both goods and services, now uniformly referred to as “GROSS SALES” across various transactions.

- Invoice: The act standardizes documentation, replacing various sales documents with a single “INVOICE” format for goods and services.

- Billings for Sales of Service on Account: Reflects the shift to an accrual basis by changing the terminology from receipts or payments to “BILLING” or “BILLED” as appropriate.

- VAT-exempt Threshold: The VAT-exempt threshold update mechanism has been revised to adjust based on the Consumer Price Index (CPI) every three years, maintaining relevance with economic changes.

- Filing and Payment: Mandates electronic filing of tax returns and allows manual filing only when electronic platforms are unavailable. Payments must follow suit, with a preference for electronic methods.

Section 3: Specific Amendments to Sale or Exchange of Service (Sections 4.108-1, 4.108-4, and 4.108-6)

- Sec. 4.108-1: Clarifies that all services and lease of properties are subject to a 12% VAT based on gross sales.

- Sec. 4.108-4: Defines “Gross Sales” in the context of services, including all forms of compensation and materials supplied with the services, exclusive of VAT.

- Sec. 4.108-6: Details allowable deductions from gross sales for VAT computation, such as service value adjustments where refunds or credits are issued within the same quarter.

Section 4: Specific Amendments to VAT-Exempt Transactions (Section 4.109)

The amendment includes a new VAT-exempt threshold and outlines specific exemptions for small businesses and self-employed individuals whose gross annual sales do not exceed P3,000,000.00, adjusted every three years for inflation.

Section 5: Specific Amendments to Tax Credits (Section 4.110-9)

Outlines the conditions under which businesses can claim an output VAT credit on uncollected receivables, such as the necessity of a written agreement on payment terms and proper sales reporting in the Summary List of Sales.

Section 6: Specific Amendments to Claims for Refund/Tax Credit Certificate of Input Tax (Section 4.112-1)

This section extensively revises the conditions and processes for claiming refunds or tax credit certificates, including:

a. Eligibility for zero-rated and effectively zero-rated sales, b. cancellation of VAT registration, c. The procedure for filing claims, d. A defined 90-day period for the Commissioner to process claims, e. A risk-based approach to audit and verify claims, f. manner of giving a refund, g. Provisions for automatic appropriation of funds to support VAT refunds and quarterly reports.

Section 7: Transitory Provisions

Addresses how transactions made before the regulation’s effectivity are handled, specifying that VAT for billed but uncollected services and goods will be recognized upon collection.

Conclusion

RR No. 3-2024 introduces reforms aimed at simplifying the VAT and Percentage Tax processes, enhancing clarity, and ensuring tax compliance is less burdensome. These changes reflect a move towards a more streamlined and technologically integrated tax system, benefiting many taxpayers, particularly small businesses and self-employed individuals.

UHY M.L. Aguirre & Co. CPAs or Babylon2K are just a click away for further clarity or assistance.

Whether you’re an entrepreneur, a remote employee, or a small business owner, Babylon2k offers a customized service that meets your needs. Each service has a corresponding code (e.g., 110010, 110040).

Babylon2k’s tax and compliance services can help you navigate your finances effectively. Our team of experts will guide you toward informed financial decisions that lead your business to success. We offer:

- Tax Filing and Compliance (ITR preparation packages, 1709 preparation, Tax compliance review & planning, U.S. Tax return preparation and filing, etc…) – Service Codes: GG0010, GG0040, GG0130, GG0170, etc.

When you’re ready to get started, simply request a quote and enter the relevant service code(s) to ensure we can connect you with the perfect Babylon2k specialist for your needs.

Do you want to know more about how we can help? It’s easy!

- Tutorial on Requesting a Quote: https://babylon2k.tawk.help/article/express-request-for-quote

- Schedule a FREE DEMO & CONSULTATION: https://bit.ly/b2k-demo.

- Contact Babylon2k through our chatbot or Viber/Whatsapp Number @ +63-927-945-3382.

- Email Babylon2k directly at [email protected]

- Directly Message us on LinkedIn

For easy reference, a copy of RR 3-2024 is enclosed for your reading pleasure.