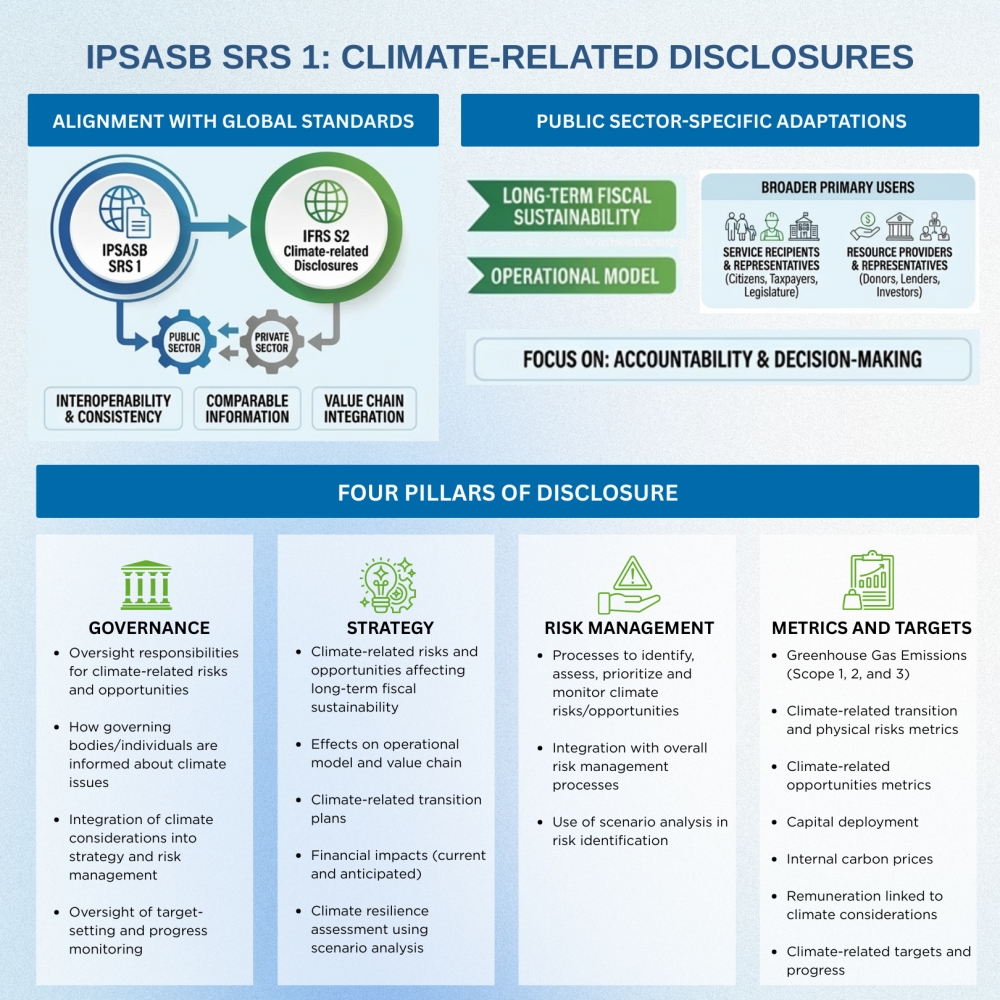

The International Public Sector Accounting Standards Board (IPSASB) recently released Sustainability Reporting Standards 1, known as Climate-related Disclosures, to provide governments and public sector entities with guidance on how to report and disclose climate-related risks and opportunities.

What Is IPSASB Sustainability Reporting Standard 1 (SRS 1)?

The IPSASB SRS 1 standard recognizes that climate change is a fiscal sustainability issue for public sector entities. By requiring transparent disclosure of climate-related risks, opportunities, and resilience, it supports:

- Better decision-making by governments and other public sector entities

- Enhanced accountability to citizens and other stakeholders

- More effective climate action globally

- Sustainable public finances for current and future generations

The standard will take effect on January 1, 2028, but earlier application is permitted. It will be applicable to public sector entities including: National, regional, state/provincial, and local governments; Government ministries, departments, programs, boards, commissions, and agencies; Public sector social security funds, trusts, and statutory authorities; and International governmental organizations.

Philippine Perspective: COA’s Role in Shaping IPSASB SRS 1

When the IPSASB was drafting the standard, the Commission on Audit provided its recommendations and comments on the proposed exposure draft last February 2025. A copy of COA’s recommendations can be accessed here. It is interesting to note that the final version of IPSASB SRS 1 addressed the majority of the recommendations provided by COA.

The key changes include:

- Scope 3 transition extended from 1 to 3 years – directly addressing complexity concerns

- Broader risk considerations – economic and social impacts now explicitly included

- Robust proportionality mechanisms – addressing varying capacity levels

- Enhanced implementation guidance – examples and best practices added

The COA and the Governance Commission for Government Owned and Controlled Corporations (GCG) will most likely spearhead the adoption of IPSASB SRS 1 in the PH public sector. Such adoption will transform climate reporting from voluntary to systematic in the public sector, while recognizing diverse capacity levels and enabling progressive improvement over time. It can likewise drive meaningful climate action through transparency and accountability.

Build Climate Reporting Proficiency with Confidence

The release of the IPSASB Sustainability Reporting Standard 1 signifies a shift in how public-sector entities should address climate-related threats and opportunities. By treating climate change as a factor in fiscal sustainability, the Standard lays the foundation for more consistent, transparent, and impactful climate disclosures.

Reach out to Babylon2k to support your IPSASB SRS 1 adoption: From gap assessments and policy development to implementation roadmaps and capacity-building training — our team is ready to help public sector entities comply proportionately, strengthen governance, and turn climate disclosures into meaningful action.